Sorry, nothing in cart.

Best Buy Or Ulta Beauty: Which Retailer Has More Upside Potential?

- By michael@cvcteam.com

- |

The temporary closure of retail stores during the coronavirus pandemic had a severe impact on the retail sector. However, a spike in e-commerce sales helped retailers to offset part of the loss of sales from the closure of physical stores. Many US retailers are recovering with the gradual reopening of stores since May. Meanwhile, investors will be keenly watching sales trends as the peak holiday season approaches.

Using the TipRanks’ Stock Comparison tool, we will place consumer electronics retailer Best Buy and beauty retailer Ulta Beauty alongside each other to see which stock offers a better investment opportunity.

Best Buy (BBY)

Thanks to remote working and shelter-at-home orders, Best Buy experienced strong sales in the second quarter of fiscal 2021 (ended Aug.1) for certain consumer electronics categories even as stores were open by appointment only for the first six weeks of the quarter and demand shifted to online channels.

The specialty retailer’s 2Q revenue grew 3.9% Y/Y to $9.91 billion with comparable sales (or comps) rising 5.8% and domestic online comps surging 242%. Adjusted EPS jumped 58.3% to $1.71. Merchandise categories that experienced strong growth included computing, appliances and tablets. But mobile phones and digital imaging sales declined.

Despite strong 2Q performance, investors were disappointed as the company cautioned that although it expects Y/Y growth in 3Q revenue, the 20% growth level seen in the first three of weeks of 3Q might not continue at this rate in the remainder of the quarter. In addition, the company indicated that looking ahead, its 2Q earnings growth rate might not be sustainable due to more labor hours in the physical stores, reinstatement of short-term incentive plans and higher advertising spend in 3Q.

Best Buy also pointed to uncertainty related to its performance in the second half of the year due to several factors, including the government’s stimulus actions, shift in personal spending from travel and dining out and the impact and duration of the pandemic.

Overall, Best Buy’s strong online business and its exposure to the in-demand consumer electronics categories helped the company weather the current crisis better than other retailers. However, higher costs to meet the demand for increased online sales are still a concern.

On Sept. 1, Loop Capital Markets analyst Anthony Chukumba reiterated his Buy rating on the stock with a price target of $130 following research into the company’s product pricing compared to Amazon. The analyst compared prices of 50 items across 5 different product categories and found that Best Buy’s prices are getting more competitive.

The results showed that Best Buy was 2.4% more expensive than Amazon, and that figure was an improvement from the 3.6% rate that the analyst previously observed in June. Chukumba believes that a narrowing price gap is good news for Best Buy. He adds that the slightly higher prices are less likely to put consumers off, especially if they want the convenience of picking up an item in-store or curbside. (See BBY stock analysis on TipRanks)

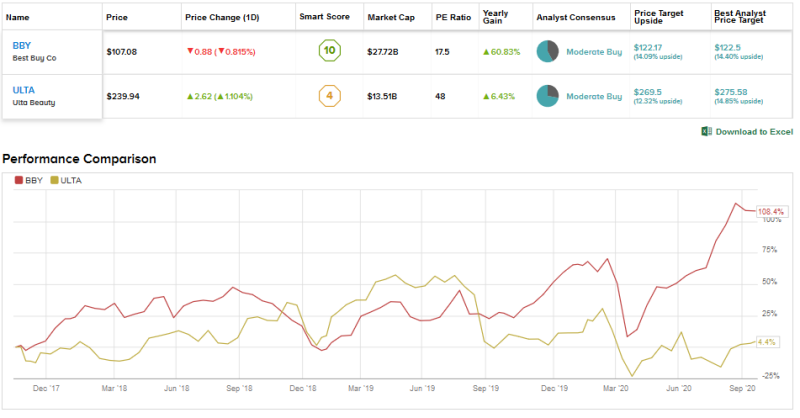

Meanwhile, the Street has a Moderate Buy analyst consensus on the stock that breaks down into 11 Buys, 8 Holds and no Sell ratings. With shares up about 22% so far this year, the average analyst price target of $122.17 reflects upside potential of another 14% in the coming months.

Leave a Reply